CommScope Holding Company, Inc. (COMM): Investment Analysis of Q2 2025 Earnings Expectations (Aug 7th, 2025)

A Pre-Earnings Risk/Benefit Assessment for Investors - July 23, 2025

Pre-Earnings Company Summary

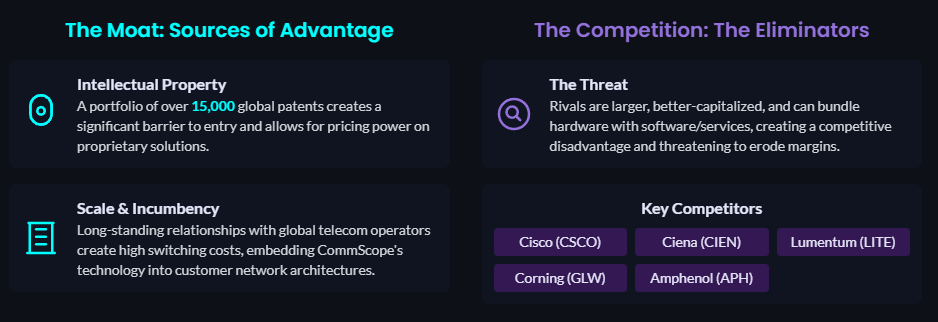

CommScope provides critical network infrastructure solutions for telecom operators and enterprise customers. The company's core business involves designing and manufacturing the hardware enabling digital communication, from fiber and coaxial cables to data center connectivity. Its market position is that of a scaled incumbent with a significant patent portfolio, but it faces intense pressure from better-capitalized competitors like Cisco Systems (CSCO), Ciena (CIEN), and Lumentum (LITE).

What's Unique: Competitive Moat vs. Market Reality

CommScope's competitive advantage is built on two pillars: a massive intellectual property portfolio and its entrenched status as a scaled, incumbent supplier. This moat, however, is under constant assault from larger, better-capitalized competitors who can leverage their financial strength to erode margins and bundle competing services, creating the core strategic tension for the company.

Executive Summary

The upcoming Q2 earnings report on July 30th is a pivotal event that will either confirm the AI-driven growth thesis established in Q1 or force the market to refocus on the company's overwhelming debt burden. The stock is positioned for a binary outcome.

Anticipated Impact

Potentially Thesis-Altering. The results will validate or invalidate the sustainability of the AI growth narrative, which is the primary pillar of the bull case against the company's significant financial leverage.

Key Question for this Report

Was the explosive 88% growth in the enterprise fiber business a one-time surge driven by specific projects, or is it the beginning of a durable, high-growth trend that can fundamentally alter the company's financial trajectory?

The Bull Case: What Needs to Happen on July 30th

For the bull thesis to gain traction, the Q2 report must provide definitive proof that the momentum from Q1 is not just sustainable but accelerating. This requires strong quantitative results and confident forward-looking commentary that reinforces the AI growth narrative and demonstrates a clear path to de-leveraging the balance sheet.

Sustained Hyper-Growth

Bulls need to see enterprise fiber revenue growth remain exceptionally strong, ideally above 50% year-over-year, to confirm the AI demand pipeline is robust and not a one-quarter anomaly.

Margin Durability

Core Adjusted EBITDA margins must remain above 20%. This would prove the 1,150 bps expansion in Q1 was due to structural operating leverage, not temporary factors, signaling powerful cash flow generation potential.

Continued Backlog Growth

The CCS segment backlog must show another sequential increase. This would provide forward visibility and tangible evidence that demand is outpacing the company's ability to supply, a strong indicator of pricing power.

Upgraded Full-Year Guidance

The most powerful bull signal would be an increase to the full-year 2025 Core Adjusted EBITDA guidance of $1.00-$1.05 billion, indicating management's supreme confidence in the second half of the year.

The Bear Case: Potential Negative Surprises

The bear case will be validated if the Q2 report reveals that Q1's stellar performance was a peak. Any signs of decelerating growth, margin compression, or cautious management commentary would immediately shift the focus back to the company's precarious financial health and its inability to escape its debt burden.

Sharp Growth Deceleration

A significant slowdown in enterprise fiber growth would confirm bears' suspicions that Q1 was an outlier. This would undermine the entire AI narrative and reframe CommScope as a low-growth, cyclical business.

Margin Mean Reversion

If EBITDA margins compress back towards the historical average, it would imply that the Q1 profitability surge was unsustainable. This would have severe negative implications for free cash flow projections and debt repayment capacity.

Cautious Forward Guidance

Any cautious language regarding second-half demand, particularly citing weakness in telecom capex or pricing pressure from competitors, would validate the core tenets of the bear thesis and likely lead to analyst downgrades.

Negative Inventory Commentary

A reversal of Q1's claim that inventory destocking is "behind us" would be a major red flag, suggesting that visibility into end-market demand is poor and that another cyclical downturn is possible.

Pre-Earnings Synthesis: The Binary Outcome

The investment case for CommScope heading into earnings is a sharply defined balance between a potentially transformative growth story and a crippling financial reality. The probability model's near-50% result numerically confirms this equilibrium. The stock is priced for a significant move, and the Q2 report will almost certainly provide the direction.

__

Report Date: July 23, 2025. This analysis is for informational purposes only and does not constitute investment advice. Information sourced from data provided for this analysis. All financial projections and opinions are subject to change. Conduct your own due diligence.